How Blockchain Works Explained Simply

Blockchain technology serves as a revolutionary way to record transactions. It functions as a decentralized digital ledger, ensuring transparency and security. Each transaction is grouped into blocks, which are then linked to create an unchangeable chain. This process involves network participants who verify the accuracy of each entry. Understanding how these components interact can illuminate the broader implications of blockchain for various industries. What lies beyond the basics of this technology?

What Is Blockchain?

Blockchain is a revolutionary digital ledger technology that facilitates secure and transparent record-keeping across multiple participants.

By utilizing a decentralized ledger, it eliminates the need for intermediaries, empowering users with greater control over their transactions.

This innovation underpins digital currency systems, allowing for peer-to-peer exchanges without centralized oversight.

Ultimately, blockchain fosters financial freedom and enhances trust in digital interactions.

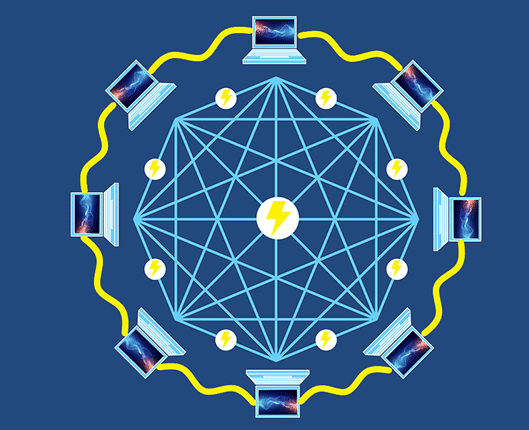

Key Components of Blockchain

At the heart of blockchain technology are several key components that work together to ensure its functionality and security.

A decentralized ledger records all transactions transparently, promoting trust among users.

Additionally, cryptographic security safeguards data against unauthorized access and tampering, allowing individuals to maintain control over their information.

Together, these components create a robust framework that embodies the principles of freedom and transparency.

See also: How Data and Technology Are Modernizing Horse Racing

How Transactions Are Verified

Numerous mechanisms are employed to verify transactions within a blockchain network, ensuring accuracy and security.

Transaction validation occurs through consensus mechanisms, where participants in the network agree on the legitimacy of transactions.

Various methods, such as proof of work and proof of stake, facilitate this agreement, preventing fraud and maintaining the integrity of the blockchain, ultimately fostering trust among users.

Benefits of Using Blockchain

A range of benefits emerges from the adoption of blockchain technology, making it an attractive solution for various industries.

Its security features significantly enhance data protection, reducing risks associated with fraud and cyberattacks.

Additionally, the decentralized system promotes transparency and trust among participants, eliminating the need for intermediaries.

This empowerment fosters greater freedom for users, streamlining processes and reducing costs in transactions.

Conclusion

In a world where trust is often elusive, blockchain emerges as the superhero of digital transactions, wielding the power of transparency and security. With its decentralized fortress guarding every block of information, it eliminates the need for intermediaries and their potential mischief. Imagine a realm where every transaction is etched in stone, immune to tampering. The benefits of blockchain are not just revolutionary; they are the dawn of a new era in trust and accountability that could reshape our entire digital landscape.